EY Law LLP is a Canadian law firm, affiliated with Ernst & Young LLP in Canada. Both EY Law LLP and Ernst & Young LLP are Ontario limited liability partnerships. For more information about the global EY organization please visit www.ey.com.

Recent Searches

Tax Alert 2022 No. 42, 3 November 2022

“I know that times feel tough. The north wind is blowing. But we have a well-built house with a solid roof, and we have survived far colder winters before. And just as fall turns to winter, so, too, does winter turn to spring. There are warmer days ahead, and we will reach them together. By building an economy that works for everyone.”

Deputy Prime Minister and Finance Minister Chrystia Freeland

Economic and Fiscal Update 2022

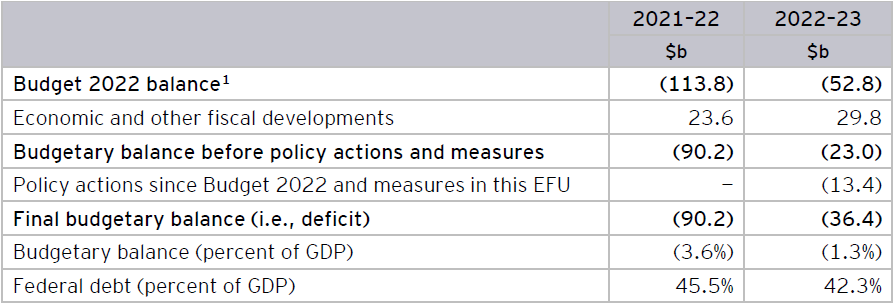

On 3 November 2022, federal Deputy Prime Minister and Finance Minister Chrystia Freeland tabled the federal government’s Economic and Fiscal Update 2022. The Economic and Fiscal Update 2022 (EFU) contains several tax measures affecting individuals and corporations. As set out in Table A, the minister anticipates a deficit of $36.4b for 2022–23 and projects deficits for each of the next four years and a surplus of $4.5b for 2027–2028 (under a baseline scenario).

In addition, on 3 November 2022, the government also tabled a notice of ways and means motion (NWMM) to implement certain measures announced in the EFU and certain provisions of the 2022 federal budget (Budget 2022). At the time of writing, the NWMM had not been made available.

On the same day, revised legislative proposals were also released on the excessive interest and financing expenses limitation (EIFEL) rules to take into account comments received since their initial release on 4 February 2022. One notable change is the effective date of the rules. It is now proposed that the EIFEL rules will apply in respect of taxation years that begin on or after 1 October 2023 (instead of 1 January 2023). Interested parties are invited to send comments by 6 January 2023. The revised rules will be discussed in an upcoming separate tax alert.

Also on 3 November 2022, legislative proposals were also released on the reporting rules for digital platforms operators that had been announced in Budget 2022. Comments on these proposals are also sought by 6 January 2023.

Finally, in order to fully assess the feedback received as part of the public consultation on mandatory disclosure rules launched 9 August 2022, the government announced that it intends to delay the coming into force date of the reporting requirements for reportable transactions and notifiable transactions until the date on which a bill implementing these changes receives Royal Assent. The coming into force date for uncertain tax treatments would remain the same as described in the August proposals (i.e., taxation years beginning after 2022, with penalties only applying after Royal Assent).

Table A: Projections of federal budgetary deficit*

Numbers represent the government’s baseline scenario and may not add due to rounding.

1 Budget 2022 was delivered on 8 April 2022. See EY Tax Alert 2022 Issue No. 23.

Business income tax measures

The following is a summary of the business support measures announced:

Corporate tax rates

No changes are proposed to the corporate income tax rates or to the $500,000 small-business income limit of a Canadian-controlled private corporation (CCPC). The enacted Canadian federal corporate income tax rates are summarized in Table B.

Table B: Federal corporate income tax rates*

* The corporate income tax rate for zero-emission technology manufacturers is reduced to 7.5% for eligible income otherwise subject to the 15% general corporate income tax rate or 4.5% for eligible income otherwise subject to the 9% small-business corporate income tax rate, applicable for taxation years beginning after 2021. The reduced tax rates will be gradually phased out beginning in 2029 and fully phased out for taxation years beginning after 2031.

** The government released draft legislative proposals on 9 August 2022 to implement a Canada recovery dividend in the form of a one-time 15% tax on bank and life insurer groups, applicable to 2021 taxable income (subject to a $1 billion exemption to be shared by group members), to be imposed for the 2022 taxation year and payable over a five-year period, as well as an additional tax on banks and life insurers at a rate of 1.5% on taxable income (subject to a $100 million exemption to be shared by group members), applicable for taxation years ending after 7 April 2022 (prorated for taxation years straddling this effective date). These proposals, which were first announced in Budget 2022, are not yet substantively enacted for financial reporting purposes.

Other business income tax measures

The minister also proposed the following business income tax measures:

Investment tax credit for clean technologies — Introduction of a refundable tax credit of either 30% or 20% on the capital cost of eligible equipment, effective for eligible equipment that is acquired and becomes available for use on or after the date of the 2023 federal budget (Budget 2023). The 30% rate will apply if certain labour conditions are met. Otherwise, a 20% rate will apply. Although the government noted the labour conditions would include the payment of prevailing wages based on local labour market conditions and the creation of apprenticeship training opportunities, additional details will be announced in Budget 2023. The credit will be phased out beginning with eligible equipment that becomes available for use in 2032, and will be completely phased out by 2035.

Eligible equipment will include the following:

- Electricity generation systems, including solar photovoltaic, small modular nuclear reactors, concentrated solar, wind and water (small hydro, run-of-river, wave and tidal);

- Stationary electricity storage systems that do not use fossil fuels in their operation, including, but not limited to, batteries, flywheels, supercapacitors, magnetic energy storage, compressed air energy storage, pumped hydroelectric energy storage, gravity energy storage and thermal energy storage;

- Low-carbon heat equipment, including active solar heating, air-source heat pumps and ground-source heat pumps; and

- Industrial zero-emission vehicles and related charging or refueling equipment, such as hydrogen or electric heavy duty equipment used in mining or construction.

Investment tax credit for clean hydrogen — Establishment of a refundable tax credit of at least 40% on eligible investments in clean hydrogen production, made on or after the date of Budget 2023 and based on the lifecycle carbon intensity of hydrogen. The level of the credit will also depend on whether certain labour conditions are met and, if certain of these conditions are not met, the maximum tax credit rate will be reduced by 10 percentage points. The credit will be phased out after 2030.

In the coming weeks, the Department of Finance will launch a consultation on how best to implement the credit. In particular, input will be sought on: an appropriate carbon intensity-based system in the Canadian context, the level of support needed for different production pathways in Canada, and how best to attach labour conditions to the credit to ensure a prevailing level of wages in the local labour market is paid and apprenticeship training opportunities are created.

Tax on share buybacks — Introduction of a 2% corporate tax on the net value of share buybacks by public corporations in Canada, similar to a measure introduced in the United States. The stated intention of this measure is to encourage corporations to reinvest their profits in their workers and businesses. The tax will be effective on 1 January 2024, with additional details to be announced in Budget 2023.

Review of Scientific Research and Experimental Development (SR&ED) tax incentive program — Originally announced in Budget 2022, the EFU confirms that the review of the SR&ED program, with the stated intention of ensuring that it is efficient and providing adequate support for taxpayers, is underway. An update will be provided in Budget 2023.

Tax measures for individuals

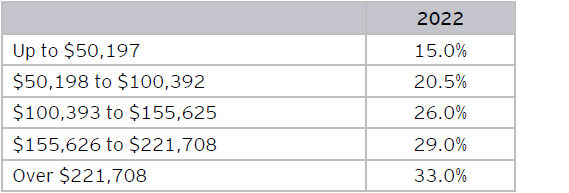

Personal income tax rates

There are no individual income tax rate or tax bracket changes in this EFU. The brackets will continue to be indexed for inflation.

See Table C for the 2022 federal rates.

Table C: Federal personal income tax rates

Other personal income tax measures

The EFU includes the following personal tax measures:

Residential property flipping rule — Budget 2022 introduced a new rule to ensure profits from flipping residential real estate are subject to full taxation and are not eligible for capital gains treatment or the principal residence exemption. The government published draft legislation to implement this proposal on 9 August 2022 and the new rule will apply to dispositions occurring on or after 1 January 2023. Under this proposal, profits (i.e., gains) that arise from the disposition of residential real estate (including a rental property) that was owned for less than 12 months will, subject to exceptions for certain life events, be deemed to be business income (which is not eligible for the 50% capital gains inclusion rate). Where the new deeming rule applies, the principal residence exemption will not be available.

The EFU proposes to expand the new property flipping rule to cover profits from assignment sales, applicable to transactions occurring on or after 1 January 2023. Profits from the disposition of rights to purchase residential property would also be treated as business income (and would not be eligible for capital gains treatment) if the rights were held for less than 12 months before disposition, subject to the exceptions for certain life events. If a purchaser holds a right to purchase (under a purchase and sale agreement) a residential property and proceeds with the purchase of the residential property, the 12-month holding period resets on the date of the property purchase. The property flipping rule may then apply if the residential property is disposed of within 12 months of its acquisition.

If the new deeming rule does not apply because of one of the legislated exceptions, or because the property was owned for 12 months or more, it will be a question of fact as to whether the profits from the disposition are taxed as a capital gain or as business income.

Canada workers benefit — The EFU proposes to automatically provide advance quarterly Canada workers benefit (CWB) payments to individuals who qualified for the CWB in the prior taxation year, beginning in July 2023 for the 2023 taxation year. Currently, the CWB is delivered through the filing of an individual’s personal tax return, unless (under a little-used option) the individual applied to receive up to half of their anticipated CWB entitlement through up to four advance payments. Under the proposed changes, an individual would automatically receive half of their estimated CWB entitlement for a year, determined based on their income reported in the prior year’s tax return (and where applicable, that of their spouse or common-law partner), through advance payments in July, October and January, and any additional entitlement for the year would be provided when their tax return for the year is filed. To qualify for the advance quarterly payments, an individual’s personal income tax return for the prior year must be received and assessed by the Canada Revenue Agency (CRA) before November of the current year. Eligibility for advance payments would cease if an individual moves out of the country, is incarcerated for a period of 90 days or more, or dies prior to July.

Alternative minimum tax — The EFU confirms the government’s intention to propose a new minimum tax regime (as announced in Budget 2022), and indicates that details will be released as part of Budget 2023.

Incorporated employees — The CRA is engaged in education and awareness efforts with respect to compliance with the tax rules for incorporated employees. The government will provide more information on this topic as part of Budget 2023.

Learn more

For more information, please contact your EY or EY Law advisor.

Download this tax alert

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.