EY Law LLP is a Canadian law firm, affiliated with Ernst & Young LLP in Canada. Both EY Law LLP and Ernst & Young LLP are Ontario limited liability partnerships. For more information about the global EY organization please visit www.ey.com.

Recent Searches

Tax Alert 2022 No. 30, 16 May 2022

On 28 April 2022, Bill C-19, Budget Implementation Act, 2022, No. 1 received first reading in the House of Commons. Bill C-19 implements the measures contained in the detailed Notice of Ways and Means Motion that was tabled on 26 April 2022 and contains certain tax measures announced in the 2022 federal budget and the 2021 federal budget, as well as various other measures.

The following tax alert explains in further detail the proposed measures related to the temporary expansion of immediate expensing of certain property that is acquired by a Canadian-controlled private corporation (CCPC) or certain individuals and partnerships for eligible capital cost allowance (CCA) classes.

Status of the proposals

Because of the minority status of the federal government (and despite the supply and confidence agreement between the governing Liberal Party and the opposition New Democratic Party announced on 22 March 2022), the measures contained in Bill C-19 will be considered substantively enacted for financial reporting purposes when the bill passes third reading in the House of Commons.

The Canada Revenue Agency (CRA) previously stated on its website that legislation to implement the immediate expensing incentive must be tabled in the House of Commons before eligible taxpayers can begin claiming this incentive. As such, it appears that as of 28 April 2022, eligible taxpayers may begin to claim the related deductions in their T2 return where all the conditions for the incentive are met.

Summary of the proposals

Immediate expensing incentive

The 2021 federal budget proposed to implement measures to temporarily allow for immediate expensing of up to $1.5 million per taxation year for certain classes of property acquired by a CCPC on or after 19 April 2021 that becomes available for use before 1 January 2024. These measures were designed to encourage investments by small and medium-sized Canadian businesses to accelerate economic recovery and support productivity growth in the future.

As explained below, the immediate expensing incentive, as first announced in the 2021 federal budget, was further expanded during 2022 to include immediate expensing of eligible property acquired by a Canadian-resident individual (other than a trust) or a Canadian partnership, where all the members are CCPCs or Canadian-resident individuals (other than trusts) for property acquired after 31 December 2021, that becomes available for use before 1 January 2025 (or before 1 January 2024 for partnerships where not all the members are individuals).

Broadly speaking, the new measures are available to an eligible person or partnership in respect of immediate expensing property, as defined below. Immediate expensing is available in the year in which the eligible property becomes available for use. The $1.5 million immediate expensing limit per taxation year must be shared among members of an associated group of eligible persons or partnerships and prorated for short taxation years. No carryforward will be available if the full $1.5 million immediate expensing limit is not used in a particular taxation year. The half-year rule does not apply to property for which the incentive is applied.

Taxpayers will be able to choose whether particular eligible assets are immediately expensed under this new measure or subject to regular CCA rates, and other enhanced CCA rates will continue to apply (provided the total CCA deduction does not exceed the capital cost of the property). The accelerated investment incentive continues to apply for property acquired before 2028.1

Eligible person or partnership

An eligible person or partnership (EPOP) includes CCPCs, individuals (other than trusts) resident in Canada, or Canadian partnerships where all the members are CCPCs, Canadian-resident individuals (other than a trust), or a combination thereof. To qualify as an EPOP, the person or partnership must satisfy the qualifications and maintain their status throughout the taxation year.

Multi-tiered partnerships do not meet the definition of an EPOP.

Immediate expensing property

Immediate expensing property (IEP) is property acquired by an EPOP and includes all property subject to the CCA rules, but excludes property included in the following CCA classes (generally long-lived asset classes):

- Classes 1 to 6 (e.g., buildings, greenhouses, structures);

- Class 14.1 (e.g., goodwill);

- Class 17 (e.g., surface construction such as roads);

- Class 47 (e.g., transmission or distribution equipment and structures used for transmission or distribution of electrical energy);

- Class 49 (e.g., pipelines, including monitoring devices, valves, etc. used for the transmission of oil and gas); and

- Class 51 (e.g., pipelines, including control and monitoring devices, valves, etc. used to distribute natural gas).

To qualify as an IEP, the property must be:

- Acquired after 18 April 2021 and become available for use before 1 January 2024 if the EPOP is a CCPC;

- Acquired after 31 December 2021 and become available for use before 1 January 2025 if the EPOP is a Canadian-resident individual or a partnership where all the members are individuals; or

- Acquired after 31 December 2021 and become available for use before 1 January 2024 if the EPOP is a partnership where not all members are individuals.

In addition, property that has been used, or acquired for use, for any purpose before being acquired by the EPOP may be IEP provided certain conditions, similar to those enacted for accelerated investment incentive property under Regulation 1104(4)(b), are met.

However, special rules prevent immediate expensing of certain property transferred from a non-arm’s length person if the expenditures related to the transferred property were made prior to the acquisition dates outlined above for an EPOP.

Designated immediate expensing property

The immediate expensing incentive is available for property designated as designated immediate expensing property (DIEP). To be eligible as DIEP, the property must satisfy the following three conditions:

- Qualify as IEP of an EPOP;

- Become available for use in the taxation year; and

- Be designated as DIEP by the EPOP in prescribed form filed with the minister for the taxation year.

The designation must be filed on or before the day that is 12 months after the EPOP’s filing due date for the taxation year to which the designation relates. If the EPOP is a partnership, the designation must be filed on or before the day that is 12 months after the day on which any member of the partnership is required to file an information return under section 229 of the Income Tax Regulations (Regulations) for the period to which the designation relates.

The immediate expensing incentive is limited to the least of:

- The EPOP’s immediate expensing limit2 for the taxation year (i.e., generally $1.5 million, subject to the allocation requirements among an associated group);

- The undepreciated capital cost (UCC) of the DIEP to the EPOP, before claiming any CCA deductions for the taxation year; and

- If the EPOP is not a CCPC, the EPOP’s income (before claiming any CCA deductions for the taxation year), if any, earned from the business or property in which the relevant DIEP is used for the taxation year.

Consequently, an individual or partnership cannot use the immediate expensing incentive to create or increase a loss for an individual or a partnership.

If the capital cost of IEP in a taxation year exceeds the EPOP’s immediate expensing limit and the IEP is included in more than one CCA class, the EPOP may designate to which CCA class the immediate expensing incentive is allocated. For example, an EPOP may allocate their immediate expensing limit to CCA classes with lower depreciation rates to maximize the benefit of the tax deferral. Any remaining UCC will be eligible for additional CCA deductions under the existing CCA rules, including the other enhanced deductions (such as the full expensing for manufacturing and processing machinery and equipment and for clean energy equipment). Consequently, an EPOP (and its associated group, if any) may benefit from the $1.5 million immediate expensing incentive in addition to all other available CCA claims under the current rules as long as the total CCA deduction claimed does not exceed the capital cost of the property.

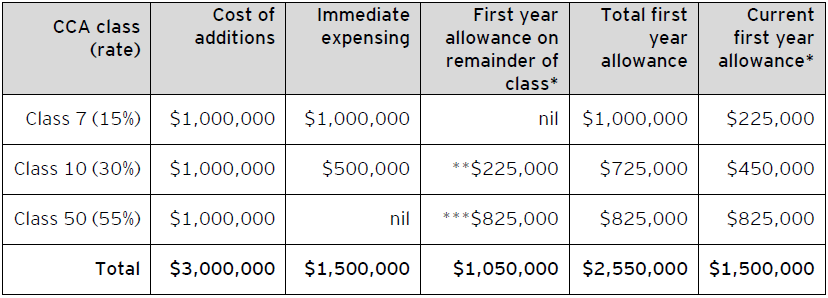

The following example, adapted from the Department of Finance explanatory notes, illustrates how the rules apply.

Facts and assumptions:

ACo, a CCPC, is an EPOP for purposes of the immediate expensing incentive. ACo invests $3 million in equal amounts to acquire three properties: one in CCA Class 7 (15%); one in CCA Class 10 (30%); and one in CCA Class 50 (55%). All properties become available for use in the year in which they are acquired. ACo is not associated with any other EPOP; as such, its immediate expensing limit is $1.5 million for the year. The income derived from the source in which the properties are used by ACo exceeds $1.5 million for the year, and ACo holds no other Class 7, 10 or 50 properties.

While ACo may designate any of the three properties as DIEP, it is reasonable to assume that ACo would generally designate property that falls under CCA classes with the lowest CCA depreciation rate.

Tax consequences:

ACo would be allowed to claim a total first-year deduction of up to $2,550,000 rather than a deduction of $1,500,000 under the existing rules, as illustrated in the table below, resulting in an additional deduction of $1,050,000 in the year due to the immediate expensing incentive.

* It is assumed that the property is eligible for the enhanced first-year CCA allowance under the accelerated investment incentive property rules.

** Computed as enhanced first-year CCA rate of 45% (i.e., 30% * 1.5) * $500,000 (i.e., remaining UCC in Class 10 after the immediate expensing incentive) = $225,000.

** Computed as enhanced first-year CCA rate of 82.5% (i.e., 55% * 1.5) * $1,000,000 = $825,000.

Immediate expensing limit

Specific provisions address the allocation of the $1.5 million limit among the associated EPOP members. The rules generally operate in a similar manner as the rules governing the allocation of the small business deduction limit in section 125 of the Income Tax Act (the Act); however, they also include important additional requirements.

The associated group of EPOPs must inform the minister of their allocation of the immediate expensing limit in prescribed form using the following two-stage process:

- The associated EPOPs will assign to one or more of their members a percentage, ensuring that the total of the percentages assigned to each member does not exceed 100%. If the total exceeds 100%, the immediate expensing limit of the associated EPOP group will be nil. The EPOPs must file an agreement, in prescribed form, with the minister for the percentage allocation to have effect.

- Each associated EPOP to which a percentage of the immediate expensing limit has been assigned must multiply that percentage by $1.5 million.

Special rules apply to determine whether two or more EPOPs are associated with each other within the meaning of section 256 of the Act.3 Specific provisions also govern the computation of the immediate expensing limit where an EPOP in an associated group has two or more taxation years ending in a calendar year.4

Other considerations

The existing rules restricting the amount of CCA that may be claimed in certain circumstances (such as the leasing property rules, rental property rules, specified leasing property rules and specified energy property rules) will continue to apply.

Implications

The rules for the immediate expensing incentive are not yet law and are therefore subject to amendment. However, according to the CRA’s website, as of the date draft legislation is tabled in the House of Commons, i.e., 28 April 2022, taxpayers can begin to claim the incentive. Amended tax returns will need to be filed where property was acquired prior to 28 April 2022 and qualifies for the incentive, depending on whether the EPOP is a CCPC, a Canadian resident individual or partnership where all members are individuals, or a partnership where not all members are individuals.

As per the draft rules, the designation must be filed on or before the day that is 12 months after the EPOP’s filing due date for the taxation year to which the designation relates. Therefore, under the current proposals, an eligible CCPC’s amended tax returns must be filed prior to 18 months after its taxation year-end in order to qualify for the immediate expensing incentive. If the EPOP is a partnership, the designation must be filed on or before the day that is 12 months after the day on which any member of the partnership is required to file an information return under section 229 of the Regulations for the period to which the designation relates.

Accordingly, it would be prudent to start to assemble relevant information at this time. To learn about future developments, or for more information or assistance, please contact your EY tax advisor.

Learn more

For more information on the 2021 federal budget measures, refer to EY Tax Alert 2021 Issue No. 19, Federal budget 2021–22: A recovery plan for jobs, growth and resilience. For other matters discussed in this Alert, contact your EY or EY Law tax advisor or one of the following professionals:

Susan Bishop

+1 416 943 3444 | susan.g.bishop@ca.ey.com

Krista Robinson

+1 514 879 2783 | krista.robinson@ca.ey.com

Martin McLaughlin

+1 416 932 5751 | martin.mclaughlin@ca.ey.com

Brett Copeland

+1 902 421 6261 | brett.copeland@ca.ey.com

_____________________

[1] For additional information on the accelerated investment incentive, see EY Tax Alert 2018 Issue No. 40 , Federal Fall Economic Statement announces significant acceleration of CCA for most capital investments, and EY Tax Alert 2019 Issue No. 15, CCA acceleration measures substantively enacted as part of 2019 budget implementation bill.

[2] As defined in proposed subsection 1104(3.1) of the Regulations.

[3] See proposed subsection 1104(3.6) of the Regulations.

[4] See proposed subsection 1104(3.5) of the Regulations.

Download this tax alert

Budget information: For up-to-date information on the federal, provincial and territorial budgets, visit ey.com/ca/Budget.