EY Law LLP is a Canadian law firm, affiliated with Ernst & Young LLP in Canada. Both EY Law LLP and Ernst & Young LLP are Ontario limited liability partnerships. For more information about the global EY organization please visit www.ey.com.

Recent Searches

Tax Alert 2022 No. 06, 22 February 2022

The 2021 federal budget proposed a temporary reduction in the corporate income tax rate for qualifying zero-emission technology manufacturers, applicable for taxation years beginning after 2021.

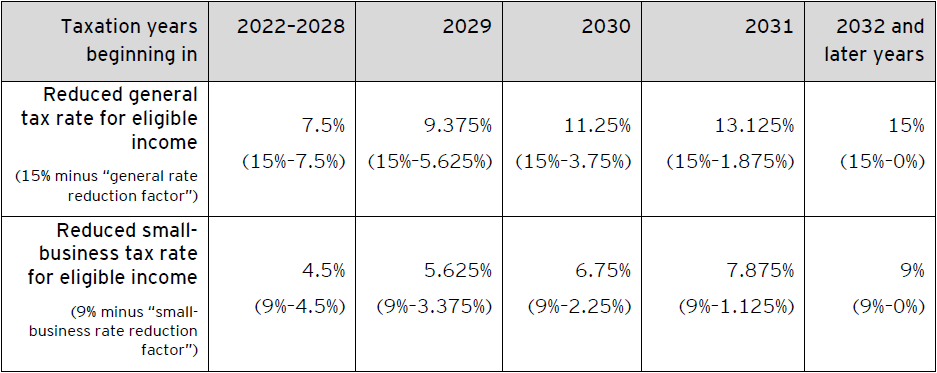

Specifically, a reduced tax rate of 7.5% will apply to eligible zero-emission technology manufacturing and processing (M&P) income that would otherwise be subject to the 15% general corporate income tax rate, and a reduced tax rate of 4.5% will apply to eligible zero-emission technology M&P income that would otherwise be subject to the 9% small-business corporate income tax rate. The reduced tax rates will be gradually phased out for taxation years beginning in 2029 and fully phased out for taxation years beginning after 2031.

Draft legislation for the proposed rate reduction (to be provided under proposed section 125.2 of the Income Tax Act) was included in a package of draft legislative proposals released for public comment by the Department of Finance on 4 February 2022. Refer to EY Tax Alert 2022 Issue No. 03.

Interested parties are invited to provide comments on the draft legislation on the proposed rate reduction by 7 March 2022.

The following is a summary of the eligibility criteria and mechanics for the proposed rate reduction, as set out in the draft legislation.

Eligible taxpayers

The proposed rate reduction is available to corporations that derive at least 10% of their gross revenue from all active businesses carried on in Canada from qualified zero-emission technology manufacturing activities.

If a corporation is a member of a partnership at any time in a taxation year, the corporation’s gross revenue (for purposes of the 10% test) will include its proportionate share of the partnership’s gross revenue from all active businesses carried on in Canada and, accordingly, from qualified zero-emission technology manufacturing activities for the year. The corporate member’s proportionate share of the partnership’s gross revenue is determined based on its share of the partnership’s income from each business for the partnership’s fiscal period coinciding with or ending in the corporation’s taxation year.

Income eligible for the rate reduction

Income eligible for the reduced tax rates is referred to as the corporation’s zero-emission technology manufacturing profits. The starting point for determining a corporation’s zero-emission technology manufacturing profits is the corporation’s adjusted business income (i.e., the total amount of the corporation’s income (net of losses) from all active businesses carried on in Canada). This adjusted business income is then prorated based on the proportion of the corporation’s total labour and capital costs incurred in qualified zero-emission technology manufacturing activities (referred to as ZETM cost of labour and ZETM cost of capital). If the total of the corporation’s ZETM cost of capital and ZETM cost of labour for the year is equal to 90% or more of the corporation’s total cost of capital and cost of labour for the year, the proportion will be deemed to be 100%.

A corporation’s adjusted business income, cost of capital and cost of labour have the same meanings that apply for purposes of the M&P profits deduction rules, as defined in the Income Tax Regulations. A corporation’s ZETM cost of capital for a taxation year is the portion of the cost of capital of the corporation that reflects the extent to which each property (included in the cost of capital) was used directly in qualified zero-emission technology manufacturing activities of the corporation during the year. For example, if a property was used 50% of the time during the year in qualified zero-emission technology manufacturing activities, 50% of the capital cost of that property would be included in the ZETM cost of capital. Similarly, a corporation’s ZETM cost of labour for a taxation year is the cost of labour incurred in qualified zero-emission technology manufacturing activities. This specifically includes salaries and wages paid or payable to persons for the portion of their time they were directly engaged in qualified zero-emission technology manufacturing activities of the corporation and other amounts paid or payable to non-employees for the performance of functions that would otherwise be directly related to qualified zero-emission technology manufacturing activities of the corporation if these persons were employees.

If a corporation is a member of a partnership, separate rules are applied to determine the corporation’s proportionate share of the partnership’s cost of capital, cost of labour, ZETM cost of capital and ZETM cost of labour. Similar to the 10% test mentioned above, such corporate member’s proportionate share is determined based on their share of the partnership’s income for the partnership’s fiscal period coinciding with or ending in the corporation’s taxation year.

Qualified zero-emission technology manufacturing activities

Qualified zero-emission technology manufacturing activities (from which eligible income must be derived) will include activities such as the manufacturing or processing of energy conversion equipment (e.g., solar, wind, water and geothermal equipment), most manufacturing or processing activities related to zero-emission vehicles (including batteries, fuel cells and charging stations), and activities in connection with the production in Canada of hydrogen by electrolysis of water, as well as of gaseous, liquid and solid biofuel.

Specifically excluded from qualified zero-emission technology manufacturing activities is the manufacturing or processing of general-purpose parts or equipment that are suitable for integration into property other than a property listed as an eligible zero-emission technology-related manufactured or processed property (in paragraph (a) of the proposed definition of qualified zero-emission technology manufacturing activities). For example, the manufacturing of standard bolts that can be used in any type of equipment (whether included in the definition or not) would be excluded.

Reduced tax rates

The following table sets out the application schedule for the reduced rates and the gradual phase out.

Calculation of the deduction for the rate reduction

The rate reduction is determined under proposed subsection 125.2(1) and is applied as a deduction from income tax otherwise payable under Part I of the Income Tax Act (similar to the small-business deduction and the M&P profits deduction).

For a corporation that is not a Canadian-controlled private corporation (CCPC), the general rate reduction factor (e.g., 7.5% for taxation years beginning after 2021 and before 2029) is applied to the lesser of the corporation’s zero-emission technology manufacturing profits for the year and the corporation’s taxable income for the year (adjusted, in a similar fashion as for the M&P profits deduction, to exclude foreign business income if a foreign tax credit is available in relation to foreign taxes on that income).

For a corporation that is a CCPC, the rate reduction is applied to both the general rate income and income eligible for the small-business deduction (referred to hereinafter as “small-business rate income”) under a two-part calculation:

- Part one: The general rate reduction factor (e.g., 7.5% for taxation years beginning after 2021 and before 2029) is applied to the lesser of:

- The amount by which the CCPC’s zero-emission technology manufacturing profits for the year exceed the CCPC’s small-business rate income for the year; and

- The CCPC’s taxable income for the year adjusted, in a similar fashion as for the M&P profits deduction, to exclude the CCPC’s small-business rate income, aggregate investment income, and foreign business income if a foreign tax credit is available in relation to foreign taxes on that income.

- Part two: The small-business rate reduction factor (e.g., 4.5% for taxation years beginning after 2021 and before 2029) is applied to the lesser of:

- The CCPC’s small-business rate income for the year; and

- The amount by which the CCPC’s zero-emission technology manufacturing profits for the year (not exceeding the CCPC’s adjusted taxable income determined under Part one above) exceed the amount eligible for the general rate reduction under Part one.

However, as shown in the following example, this two-part calculation included in the draft legislative proposals does not seem to necessarily reflect the intent of the proposals as described in the 2021 federal budget. We have raised this issue with the Department of Finance and they are working to address the issue.

Example

Facts and assumptions

For its 2022 taxation year, which coincides with the calendar year, a CCPC has $700,000 in taxable income (all earned from a business carried on in Canada and assuming no investment income). The CCPC’s zero-emission technology manufacturing profits for the year are $600,000. The CCPC is not associated with any other corporations.

Tax consequences

Although one would expect the CCPC’s deduction for the rate reduction for the 2022 taxation year to be $30,000 (i.e., the total of 7.5% on the CCPC’s zero-emission technology manufacturing profits that would otherwise be subject to the 15% general corporate income tax rate ($100,000), and 4.5% on the CCPC’s zero-emission technology manufacturing profits that would otherwise be subject to the 9% small-business corporate income tax rate ($500,000)), the application of the two-part calculation instead results in a deduction of $12,000, which is the total of $7,500 (under the Part one calculation) and $4,500 (under the Part two calculation).

The Part one calculation being 7.5% x $100,000, which is the lesser of:

- $100,000 (i.e., $600,000 (zero-emission technology manufacturing profits) - $500,000 (small-business rate income)); and

- $200,000 (i.e., $700,000 (taxable income) - $500,000 (small-business rate income)).

The Part two calculation being 4.5% x $100,000, which is the lesser of:

- $500,000 (small-business rate income); and

- $100,000 (i.e., $200,000 (zero-emission technology manufacturing profits ($600,000) but not exceeding the adjusted taxable income under Part one calculation ($200,000)) – $100,000 (amount eligible for the general rate reduction under Part one calculation).

As noted above, if the corporation derives less than 10% of its gross revenue from all active businesses carried on in Canada from qualified zero-emission technology manufacturing activities, no deduction will be available to the corporation.

Allocation of corporate income for dividend distribution purposes

Due to the targeted application and temporary nature of the rate reduction, no changes are being made to the dividend tax credit rates or to the allocation of corporate income for the purpose of dividend distributions. Income subject to the reduced general corporate income tax rate will continue to give rise to eligible dividends and the enhanced dividend tax credit rate, and income subject to the reduced small-business corporate income tax rate will continue to give rise to non-eligible dividends and the ordinary dividend tax credit rate.

Financial reporting

Because of the current minority government, the rate reduction will be considered substantively enacted for Canadian financial reporting purposes when the enacting legislation receives third reading in the House of Commons. We expect this will occur during the second quarter of 2022.

Learn more

For more information on this measure, contact your EY or EY Law tax advisor.